Introduction

This is a bonus follow-up article to the Evolution of In-Store Loyalty series.

Following the publication of the series, one question repeatedly surfaced in industry conversations:

What about receipt scanning?

Receipt scanning has emerged as a widely adopted mechanism across cashback platforms and coalition loyalty programmes — particularly because it solves one important problem extremely well:

Enabling loyalty participation without requiring PoS or payment integration.

This makes it operationally scalable across fragmented merchant ecosystems.

However, structurally, receipt scanning behaves very differently from both traditional loyalty systems and Card-Linked Offers (CLOs).

While it addresses certain limitations of existing models, it introduces a distinct set of trade-offs — particularly around customer effort, fraud management, and attribution.

Where Receipt Scanning Fits in the Evolution

The evolution of in-store loyalty can broadly be understood as follows:

- Scanning loyalty cards

→ customer identifies themselves at checkout - Card-Linked Offers (CLOs)

→ transactions are detected after payment via payment infrastructure - Receipt scanning

→ proof of purchase is submitted after the transaction by the customer - Loyalty-Embedded Payments

→ loyalty logic is processed directly within the payment flow itself

Receipt scanning therefore sits in a structurally different position:

- not checkout-native

- not payment-native

- but post-purchase and proof-of-purchase driven

This distinction is important, as it fundamentally shifts where customer participation, transaction validation, and attribution occur.

How Receipt Scanning Works

The process typically follows a straightforward sequence:

- A customer completes a purchase

- The merchant issues a receipt

- The customer uploads or scans the receipt in an app

- OCR and AI systems extract transaction data, such as:

- merchant

- products purchased

- basket value

- date and time

- Rewards are then validated and applied

This model is now widely used across cashback platforms and coalition loyalty programmes.

Unlike CLOs, the payment instrument itself is largely irrelevant — the receipt becomes the primary proof mechanism.

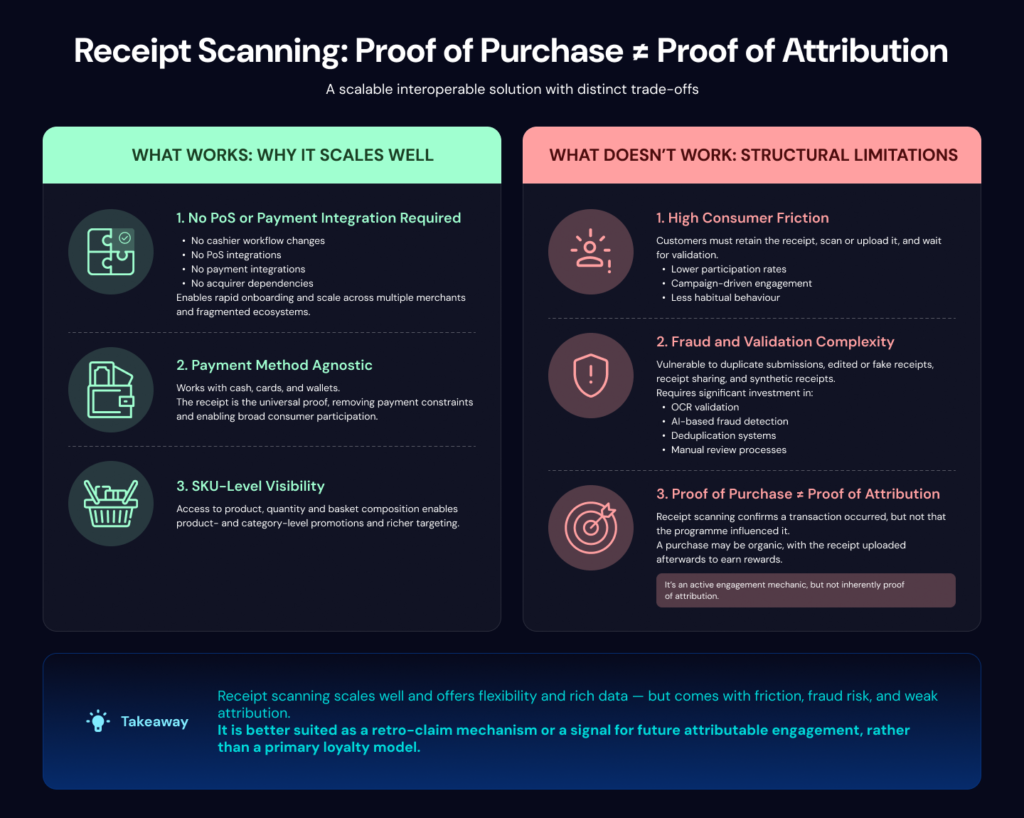

Why Receipt Scanning Scales So Well

1. No PoS or Payment Integration Required

This is the primary advantage of receipt scanning.

Unlike traditional loyalty systems, there is no need for:

- cashier workflow changes

- PoS integrations

- payment integrations

- acquirer dependencies (e.g. reliance on a specific payment acquirer)

This significantly reduces onboarding friction and operational complexity.

As a result, programmes can scale across multiple merchants and fragmented retail ecosystems with minimal infrastructure requirements.

Coalition programmes and cashback platforms, in particular, benefit from the ability to onboard merchants without requiring any integration into checkout or payment systems — as long as standard receipts are issued.

In this sense, receipt scanning functions as an interoperability layer in fragmented ecosystems.

2. Payment Method Agnostic

Receipt scanning works independently of how the customer pays.

This allows:

- cash transactions

- card payments

- digital wallets

to all qualify under the same mechanism.

Because the receipt serves as the proof of purchase, payment constraints are effectively removed — enabling broader consumer participation.

3. SKU-Level Visibility

Receipt scanning can also provide detailed basket-level insights.

A receipt may include:

- exact products purchased

- quantities

- basket composition

In contrast, many payment-based models — including traditional Card-Linked Offers — are typically limited to:

- merchant

- transaction amount

- timestamp

This enables more granular targeting and reward structuring based on actual purchase behaviour.

However, this advantage is not inherent to receipt scanning itself — it is a function of access to receipt-level data.

As digital receipt infrastructure becomes more standardised, it becomes possible to combine:

- payment-native transaction processing

with - SKU-level basket visibility from digital receipts

This creates a pathway to deliver:

- product- and category-level promotions

- without requiring manual receipt uploads

In this model, SKU-level intelligence is preserved while removing the customer friction and operational overhead associated with receipt scanning — effectively separating the data layer from the interaction model.

The strengths and trade-offs of receipt scanning become clearer when viewed side by side:

Receipt scanning delivers scale and flexibility — but introduces trade-offs around attribution, friction, and control.

The Structural Trade-Offs

Despite its scalability advantages, receipt scanning introduces a different set of structural limitations.

1. High Consumer Friction

The most immediate trade-off is customer effort.

The customer must:

- retain the receipt

- scan or upload the receipt

- wait for validation

Compared to:

- automatic CLO detection

- or embedded payment recognition

this introduces substantially higher friction.

As a result:

- participation is more selective

- engagement is more campaign-driven

- behaviour is less habitual

At the same time, this introduces an important nuance.

Receipt scanning functions as an active engagement mechanic, as the customer must deliberately submit the receipt.

However, while the action is intentional, it does not inherently establish that the purchase itself was influenced by the programme.

This distinction becomes critical when evaluating attribution.

Receipt scanning can therefore play a complementary role within merchant loyalty ecosystems — particularly as a secondary or fallback mechanism for programmes that primarily rely on:

- scanning loyalty cards

- merchant card-linked or payment-linked offers

- Loyalty-Embedded Payments

This is especially relevant as a retro-claim mechanism when customers:

- were not enrolled at the time of purchase

- did not identify themselves at checkout

- or used a non-qualifying payment method

In these cases, receipt scanning helps recover otherwise untracked transactions without requiring additional merchant infrastructure.

2. Fraud and Validation Complexity

Receipt scanning introduces a range of fraud vectors, including:

- duplicate submissions

- receipt sharing

- edited receipts

- AI-generated receipts

As a result, significant infrastructure is required for:

- OCR validation

- AI-based fraud detection

- deduplication systems

- manual review processes

Fraud prevention becomes a core operational requirement of the model.

3. Proof of Purchase ≠ Proof of Attribution

This emerged as one of the most important themes in industry discussions.

Receipt scanning provides confirmation that a transaction occurred.

It does not necessarily establish whether the programme influenced the purchase.

A customer may:

- complete a purchase independently

- and upload the receipt afterwards to receive rewards

Even though the act of submission is deliberate, the underlying transaction may still be entirely organic.

As a result, causality remains unresolved — similar to passive attribution challenges in CLO models.

Receipt scanning provides proof of purchase — not proof of attribution.

However, this also highlights where receipt scanning can be used more effectively.

Rather than rewarding the past transaction itself in cashback and coalition programmes, receipt scanning can be used to:

- signal customer intent

- identify category-level behaviour

- unlock future offers or incentives

In this model:

- the receipt becomes a behavioural input

- future engagement becomes attributable

- rewards can be linked to incremental future spend

This shifts receipt scanning from a retrospective reward mechanism toward a forward-looking engagement strategy.

Strategically, What Receipt Scanning Solves

Receipt scanning is fundamentally an interoperability workaround.

It emerged in response to:

- fragmented PoS ecosystems

- fragmented payment infrastructure

- fragmented merchant environments

Rather than integrating directly into these systems, it shifts the responsibility for transaction identification to the customer.

This trade-off enabled scalability — but at the expense of:

- seamless customer experience

- deterministic transaction participation

- strong attribution

Conclusion

Receipt scanning represents an important stage in the evolution of loyalty infrastructure.

It addresses several operational limitations of traditional loyalty systems and Card-Linked Offers — particularly around scalability, merchant onboarding, and payment flexibility.

However, its limitations are equally structural.

While it enables scalable proof of purchase, it does not inherently resolve:

- attribution

- deterministic transaction participation

- seamless, real-time engagement

Its long-term value is likely not as a standalone loyalty architecture, but as:

- a scalable interoperability layer

- a retro-claim mechanism

- and a signal for future, attributable engagement

As loyalty continues to evolve, the direction of travel increasingly points toward models where customer recognition, attribution, rewards, and redemption are processed natively within the transaction itself.