Introduction

Most loyalty models are typically explained through customer engagement mechanics — scanning loyalty cards, Card-Linked Offers, or receipt scanning.

But at a more fundamental level, loyalty models differ based on one simple question:

Who is the host — and what do they control?

Viewed through this lens, the market broadly divides into two structural categories:

- Issuer Loyalty

- Merchant Loyalty

The distinction matters because control over:

- the payment instrument,

- customer identification at checkout,

- transaction visibility,

- and reward economics

ultimately determines how a loyalty programme operates, scales, and monetises itself.

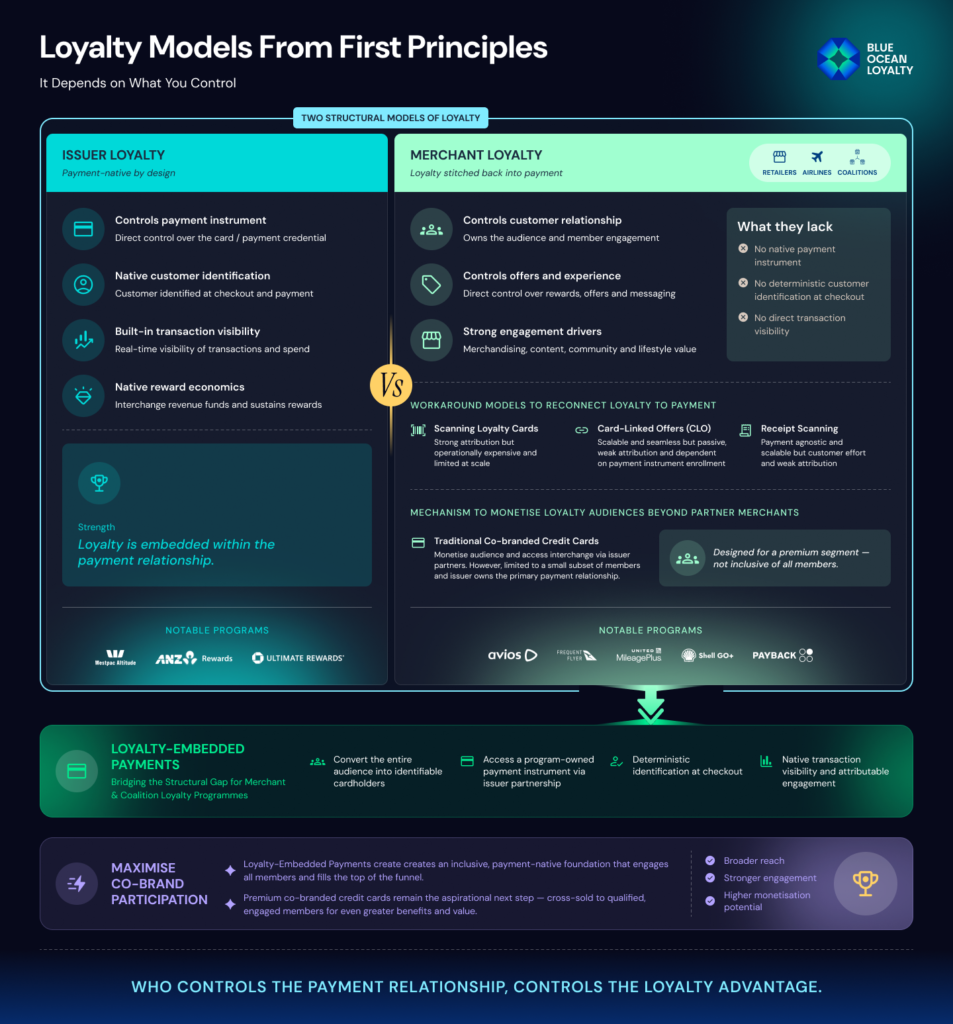

1. Issuer Loyalty

What issuers control

Issuer-led loyalty programmes — typically operated by banks and card issuers — naturally possess several structural advantages:

- Direct control over the payment instrument

- Native customer identification at checkout and payment

- Built-in transaction visibility

- Native reward economics funded through interchange revenue

This is why issuer-led rewards programmes historically became the earliest form of payment-native loyalty.

The reward mechanism is already embedded within the payment relationship itself.

Every transaction naturally generates:

- customer identity,

- transaction data,

- and interchange revenue that funds rewards.

How issuer loyalty operates

Issuer loyalty programmes therefore typically operate through:

- interchange-funded card rewards,

- with increasingly merchant-funded offers layered on top.

Merchant-funded offers are often enabled through transaction detection infrastructure such as Card-Linked Offers (CLOs).

In this model:

- customer identification,

- payment participation,

- and transaction visibility

are already solved.

The issuer’s challenge is therefore not identifying the customer or detecting the transaction.

Instead, the core challenge becomes:

Proving incrementality and attribution for merchant-funded offers.

In other words:

Did the offer genuinely influence spend — or would the transaction have occurred anyway?

2. Merchant Loyalty

Merchant loyalty includes:

- retailers,

- airline loyalty programmes,

- coalition loyalty ecosystems,

- cashback platforms,

- and broader lifestyle rewards programmes.

Unlike issuers, merchant and coalition programmes typically possess:

- strong customer relationships,

- engaged audiences,

- direct control over offers,

- and merchandising economics.

However, structurally, they lack:

- native control over the payment instrument,

- deterministic customer identification at checkout,

- and direct transaction visibility.

This creates a fundamentally different set of challenges.

How Merchant Loyalty Evolved

Because merchant loyalty programmes sit outside the payment itself, the industry evolved through two parallel categories of mechanisms:

- Customer Identification & Transaction Participation

- Audience Monetisation

A. Customer Identification & Transaction Participation

These models focused primarily on:

- customer identification,

- transaction attribution,

- and reward participation

within:

- the merchant’s own stores,

- or participating partner ecosystems.

Scanning Loyalty Cards

The earliest approach relied on customers identifying themselves at checkout through:

- loyalty cards,

- apps,

- or phone numbers.

This provided:

- strong attribution,

- reliable customer identification,

- and payment method flexibility.

But it also introduced:

- PoS integrations,

- staff dependency,

- operational friction,

- and scalability limitations.

(We explored these structural trade-offs in more detail in our earlier article: Why Scanning Loyalty Cards Is Holding Retail Back)

Card-Linked Offers (CLOs)

Card-Linked Offers attempted to remove checkout friction entirely.

Rather than identifying customers before payment, transactions were detected afterwards through payment infrastructure.

This solved:

- operational scalability,

- and checkout friction.

But introduced:

- weaker attribution,

- passive engagement,

- inconsistent transaction visibility,

- and dependence on enrolled payment instruments.

(For a deeper analysis of CLO infrastructure and attribution limitations, see: Why Card-Linked Offers Fall Short of True Loyalty and Not All Card-Linked Offers Are Built the Same)

Receipt Scanning

Receipt scanning emerged as another workaround model.

Rather than integrating into:

- checkout infrastructure,

or - payment infrastructure,

the customer simply uploads proof of purchase after the transaction.

This enables:

- scalability across fragmented merchant ecosystems,

- payment-method agnosticism,

- and SKU-level basket visibility.

But it also shifts transaction identification responsibility onto the customer.

Most importantly:

Receipt scanning provides proof of purchase — not necessarily proof of attribution.

(We explored this distinction further in: Receipt Scanning: Proof of Purchase ≠ Proof of Attribution)

B. Audience Monetisation

Merchant and coalition programmes also sought ways to monetise their audience itself — not just within participating merchant ecosystems, but against:

- issuing banks,

- payment schemes,

- and broader consumer spend.

Traditional Co-Branded Credit Cards

Co-branded credit cards emerged as the primary mechanism for this.

They enabled merchant and coalition programmes to:

- monetise customer affinity,

- participate indirectly in interchange economics,

- and extend engagement beyond their own merchant footprint.

However, traditional co-branded credit cards remained structurally limited because:

- only a small subset of members qualified,

- issuers retained primary ownership of the payment relationship,

- and the programme itself still lacked native ownership of the broader payment infrastructure.

In many ways, traditional co-branded credit cards represented an attempt by merchant loyalty programmes to partially bridge the structural advantages naturally held by issuers.

(We explored the structural trade-off between premium engagement and scalable participation in more detail in our earlier article: Why Legacy Loyalty Models Can’t Scale — and What Replaces Them)

The Structural Divide

Viewed from first principles, the loyalty landscape ultimately divides into two structural categories:

Issuer Loyalty

Programmes that natively control:

- the payment instrument,

- customer identification at checkout,

- transaction visibility,

- and reward economics through interchange revenue.

This structural advantage is why issuer-led loyalty programmes have historically delivered:

- seamless experiences,

- deterministic attribution,

- and scalable transaction-linked rewards.

Merchant Loyalty

Programmes that control:

- customer relationships,

- offers,

- and audience engagement,

but lack:

- native payment infrastructure,

- deterministic customer identification at checkout,

- and embedded transaction visibility.

As a result, merchant and coalition programmes have historically relied on:

- transaction identification mechanisms such as scanning loyalty cards, CLOs, and receipt scanning,

- alongside audience monetisation models such as traditional co-branded credit cards.

All fundamentally attempting to bridge the structural advantages naturally held by issuers.

The structural differences between issuer and merchant loyalty models can be visualised as follows:

Bridging the Structural Gap

This naturally raises a broader question:

What would it take for merchant and coalition loyalty programmes to operate with issuer-like infrastructure advantages?

In practical terms, this would mean enabling programmes to:

- convert their audience into identifiable cardholders,

- access a programme-linked payment instrument,

- recognise customers deterministically at checkout,

- and gain native transaction visibility.

This is the fundamental idea behind Loyalty-Embedded Payments.

Not by requiring brands to become licensed issuers themselves and absorb the associated regulatory complexity — but by enabling them to partner with co-brand issuers while retaining ownership of the loyalty relationship and customer engagement layer.

Conclusion

The evolution of loyalty infrastructure has largely been shaped by one underlying structural reality:

Whoever controls the payment relationship holds the strongest position in loyalty.

Issuer loyalty programmes historically held that advantage because they naturally controlled:

- the payment credential,

- customer identification,

- transaction visibility,

- and reward economics.

Merchant and coalition programmes, meanwhile, were forced to rely on expensive, fragmented, and often sub-optimal mechanisms to reconnect loyalty back into the payment itself.

From:

- scanning loyalty cards,

- to Card-Linked Offers,

- to receipt scanning,

the industry has effectively been attempting to compensate for the same structural limitation:

The lack of native payment infrastructure and deterministic customer identification at checkout.

Loyalty-Embedded Payments represent the next step in that evolution.

Not by replacing traditional co-branded credit cards — but by expanding the model itself.

Rather than limiting payment-native loyalty participation to a small subset of premium cardholders, Loyalty-Embedded Payments enable programmes to:

- convert their broader audience into identifiable co-branded reward cardholders,

- establish deterministic transaction participation at scale,

- and create a significantly larger engagement and monetisation funnel.

Once this payment-native baseline is established, programmes can begin extending beyond loyalty itself.

In this model, traditional premium co-branded credit cards continue to play an important role — but increasingly as aspirational, high-value propositions cross-sold to engaged and qualified members already actively participating within the programme ecosystem.

The same infrastructure can be used to:

- issue digital gift cards,

- enable foreign remittance,

- and distribute broader financial products such as BNPL, personal loans, auto loans, mortgages, and insurance.

In effect, the programme begins engaging, rewarding, and monetising its audience from both sides:

- against merchants through merchant-funded offers,

- and against co-brand issuers through financial products and services delivered directly within the brand experience.

This represents an important shift from traditional co-brand models, where programmes primarily handed members off to issuers for downstream cross-selling.

Instead, the loyalty programme itself increasingly becomes the engagement and distribution layer — while still leveraging the issuer for:

- regulated financial infrastructure,

- banking products,

- compliance,

- and balance sheet capabilities.

In this sense, Loyalty-Embedded Payments are not simply evolving loyalty infrastructure.

They are creating a new model where:

Loyalty, payments, merchant-funded incentives, and financial services distribution converge into a single payment-native ecosystem.